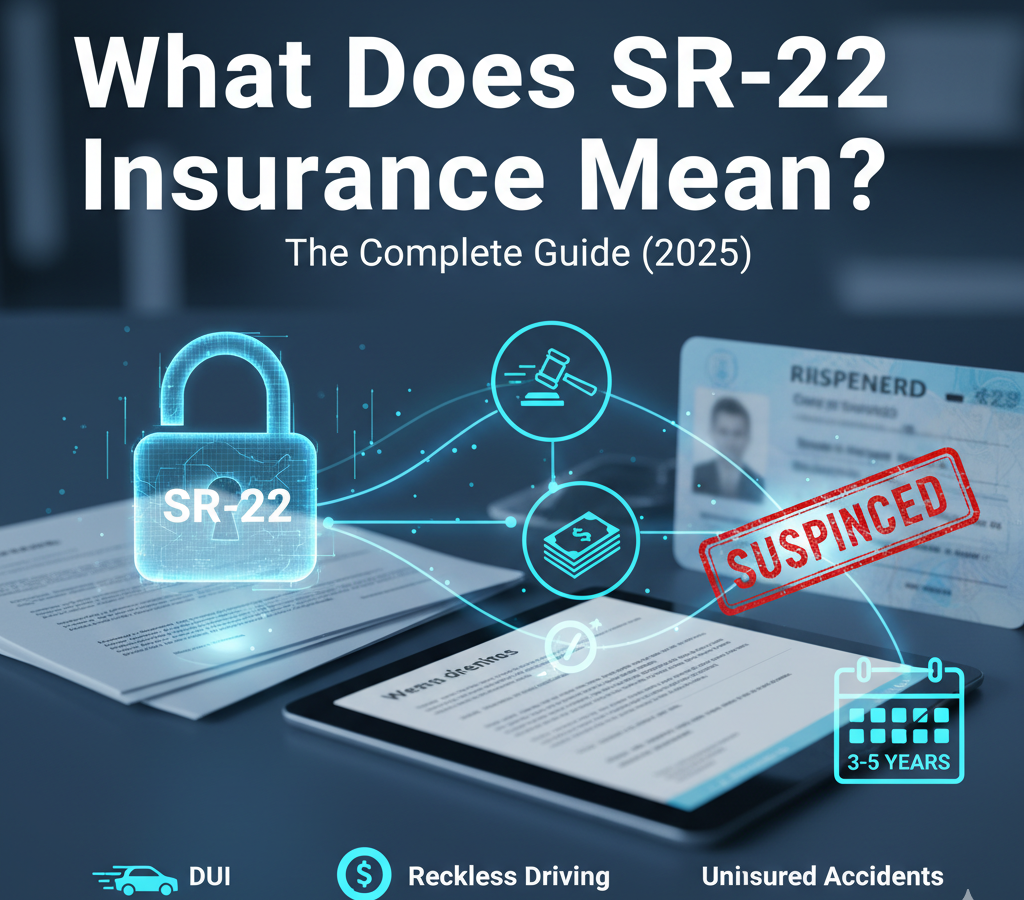

What Does SR-22 Insurance Mean? The Complete Guide (2025)

If you’ve ever had your driver’s license suspended or been told by your state that you need “SR-22 insurance,” you probably had one big question:

“What does that even mean?”

You’re not alone. Every year, thousands of U.S. drivers find themselves suddenly needing an SR-22 form and feel confused, frustrated, and worried about cost and paperwork.

This guide explains, in plain English, what SR-22 insurance really is, why you might need it, how long it lasts, what it costs, and most importantly — how to manage it without losing your license or your mind.

What SR-22 Insurance Actually Is (and Isn’t)

Let’s clear up a common misunderstanding first: SR-22 isn’t an insurance policy.

It’s a certificate — a piece of paper (or an electronic form) that your insurance company sends to your state’s Department of Motor Vehicles (DMV).

This certificate is the state’s way of checking that you have at least the minimum amount of liability insurance required by law. It proves that you’re financially responsible enough to be back on the road.

Think of it like a promise:

“Yes, this driver is insured — and if their policy ever lapses, we’ll let you (the state) know.”

The SR-22’s real name

In many states, the “SR” stands for Safety Responsibility.

That’s exactly what the state wants from you — proof that you can drive safely and cover damages if anything happens.

Why the SR-22 Exists: A Second Chance for High-Risk Drivers

SR-22 insurance isn’t about punishing drivers. It’s about rebuilding trust between you and the system.

You’re typically required to file an SR-22 when you’ve had a serious driving or insurance violation. Common reasons include:

- Driving without insurance coverage

- Being involved in an accident while uninsured

- A DUI or DWI conviction

- Reckless driving or multiple moving violations

- A license suspension or revocation

- Too many at-fault accidents in a short time

Once the court or DMV sees your SR-22, it shows you’re taking responsibility — you’ve got valid coverage and plan to maintain it.

Real Pain Points from Drivers (and Why It’s So Stressful)

If you read YouTube comments or Facebook threads about SR-22, you’ll notice the same complaints again and again:

💬 “I already have insurance, but now they’re saying I need an SR-22 too?!”

💬 “My insurance lapsed for a week, and now they’re making me start the 3-year SR-22 period all over.”

💬 “The DMV said my insurer never sent the SR-22 even though I paid for it.”

💬 “Why are my premiums double just because of a piece of paper?”

These frustrations come from how the system works. The SR-22 isn’t complicated in theory — but missing a single step (or a single payment) can create a chain reaction that leads to license suspension, extra fees, and months of stress.

How the SR-22 Filing Works (Step-by-Step)

Here’s what happens once you’ve been told you need an SR-22:

Step 1: Contact your insurer

Tell your insurance company that you need an SR-22 filing. Not all companies provide them, so you might need to switch to an insurer that does.

Step 2: The insurer files the form

Your insurer sends the SR-22 electronically to your state’s DMV. You don’t handle this yourself — the company does it for you.

Step 3: The DMV updates your record

Once the DMV receives it, your license status (suspended or restricted) begins the reinstatement process.

Step 4: You maintain continuous coverage

You must keep your insurance active for the entire SR-22 period.

If your policy is canceled or you miss a payment, your insurer will send an SR-26 form to the DMV — basically saying your coverage ended. The DMV will then likely suspend your license again.

Step 5: Completion and removal

After you’ve completed your required time (often 2–3 years), you can ask your insurer to remove the SR-22 filing from your policy and go back to normal insurance rates.

How Long You’ll Need SR-22 Insurance

Most states require you to keep the SR-22 active for 3 years.

But it depends on where you live and what the violation was.

Some states only require it for 1 year; others, especially for DUIs, might require 5 years.

The key is continuous coverage — no breaks allowed.

If your policy lapses even for a few days, the timer can reset, forcing you to start the entire period again.

🚫 A real example: One Reddit user shared,

“I was 2 months away from finishing my 3-year SR-22, then my policy got canceled by mistake. DMV made me restart the whole 3 years.”

That’s a nightmare you want to avoid. Always set up auto-pay or reminders to keep your insurance current.

How Much Does SR-22 Insurance Cost?

The SR-22 filing itself isn’t expensive — usually a $25 to $50 one-time fee.

But what really hurts is the higher insurance premium that comes with it.

Because an SR-22 means you’ve been labeled a high-risk driver, insurance companies see you as more likely to cause an accident or make a claim. As a result, they charge more.

Here’s what that looks like:

| Type of Coverage | Average Annual Premium (2025) |

|---|---|

| Standard auto insurance (clean record) | $1,800 – $2,000 |

| SR-22 required (after DUI or similar) | $3,200 – $3,600+ |

| Minimum coverage only (SR-22) | $1,500 – $2,000 |

That’s roughly 50% to 80% higher than normal rates.

Why the cost is so high:

- You’re considered a higher risk.

- Some insurers simply refuse to cover SR-22 drivers.

- You lose discounts (like safe driver or good student).

- You may have to pay upfront or in full to avoid lapses.

Types of SR-22 Filings

There are three main versions of the SR-22 certificate:

- Owner’s SR-22 – for people who own and drive their own vehicle.

- Non-owner SR-22 – for people who don’t own a car but still drive occasionally (e.g., renting or borrowing cars).

- Owner/Operator SR-22 – covers both your own cars and vehicles you drive but don’t own.

If you don’t currently own a car but need to keep your license valid, a non-owner SR-22 policy can save money since it usually costs less.

The FR-44: The SR-22’s Big Brother

In some states, namely Florida and Virginia, you’ll hear about the FR-44 form instead of SR-22.

It’s similar but comes with stricter requirements and higher liability limits (often double or more than the standard minimum).

It’s typically required for DUI-related offenses.

So if you live in Florida or Virginia, expect to pay more and maintain higher coverage levels for a longer period.

Common SR-22 Mistakes (and How to Avoid Them)

Many drivers accidentally make their situation worse. Here are the most common pitfalls — and how to prevent them:

1. Letting the policy lapse

Missing even one payment can cause an automatic suspension.

💡 Fix: Set up automatic payments and keep proof of payment handy.

2. Choosing an insurer that doesn’t file SR-22

Some companies simply don’t handle SR-22 filings.

💡 Fix: Always confirm before you buy a new policy.

3. Not confirming when the SR-22 period ends

Some drivers assume they’re done when they’re not — and get pulled over with an invalid license.

💡 Fix: Double-check with both your insurer and your DMV.

4. Canceling early after reinstatement

Even if you get your license back, canceling early restarts the process.

💡 Fix: Keep it active for the full required time, even if your record improves sooner.

5. Not updating personal information

Moved? Changed cars? New address or driver’s license number?

💡 Fix: Update your insurer immediately to avoid coverage issues.

Real Comments from U.S. Drivers (2025 Trends)

From Facebook and YouTube discussions, here’s what everyday people are saying:

“I thought SR-22 was a scam until I realized my state wouldn’t reinstate my license without it.”

“My insurance went from $120 to $290 a month overnight.”

“It’s embarrassing to even call it ‘high-risk insurance.’”

“Wish someone had told me the SR-22 is just a form — not special insurance!”

“I learned the hard way: never miss a single payment.”

These comments highlight a big truth: the confusion isn’t about the SR-22 itself — it’s about the process and communication.

Many drivers simply don’t understand what’s required, and that lack of clarity leads to more fines, suspensions, and costs.

How to Lower Your SR-22 Insurance Costs

Even though you can’t avoid the SR-22 filing requirement, there are ways to keep your premiums manageable:

- Shop around — Get multiple quotes from companies that specialize in high-risk drivers.

- Choose a higher deductible — This lowers your monthly premium (just make sure you can afford the deductible if you file a claim).

- Drive carefully — Every ticket or claim resets your progress.

- Bundle insurance policies — If you have home or renters insurance, bundle them for discounts.

- Take a defensive driving course — Some states or insurers will reduce rates if you complete one.

- Pay the premium in full — Paying upfront avoids installment fees and late payment risks.

- Ask for discounts — Some insurers still offer loyalty, paperless, or auto-pay discounts even on SR-22 policies.

Frequently Asked Questions (2025 Edition)

1. Is SR-22 insurance the same everywhere?

No. Each U.S. state has its own rules, costs, and filing process. Always check with your local DMV.

2. What happens if I move to another state?

Your SR-22 requirement follows you. You must still meet your original state’s terms, even if you move.

3. What if I don’t own a car anymore?

You can get a non-owner SR-22 policy, which keeps your license valid without owning a car.

4. Does SR-22 affect my credit score?

No. It doesn’t directly affect your credit, but late insurance payments could if they go to collections.

5. Can I get rid of SR-22 early?

Usually not. You must complete the full time period set by your court or DMV.

Life After SR-22: What Happens When It’s Over

When your required period ends — usually after 3 years — you can finally ask your insurer to remove the SR-22 filing from your policy.

Once that’s done:

- Your insurer notifies the DMV that you’ve met your obligation.

- Your license record returns to normal.

- You can switch to a regular policy again.

And the best part? Your rates will eventually go down.

It may take another 6–12 months of clean driving to see big savings, but once your high-risk label expires, you’re back to standard pricing.

The Bigger Picture: SR-22 as a Fresh Start

It’s easy to see SR-22 as a punishment. But for many drivers, it’s also a second chance.

It allows you to get back behind the wheel legally, rebuild your reputation, and prove you can handle the responsibility.

Yes — it’s more expensive.

Yes — it’s stressful.

But it’s also temporary.

Most drivers who complete their SR-22 period without issues never have to deal with it again. And once it’s over, you’ll appreciate the peace of mind that comes from staying insured, organized, and compliant.

Final Thoughts

SR-22 insurance doesn’t mean you’re a bad driver — it just means you’ve had a bump in the road.

What matters most is what you do next.

Be responsible. Pay on time. Keep your coverage active.

And use this period to rebuild your driving record and regain your financial freedom.

By understanding the process and avoiding the common pitfalls, you can move through your SR-22 period smoothly — and come out stronger, safer, and smarter on the other side.